How I bought my first apartment with 25 years old and 0€ down payment

One of the goals I set for myself with this blog is to talk openly about my investments, the things I do, the things that go right, and the things that go wrong, and some things that I have learned along the way or that I continue to learn day by day. I do this also knowing that everything related to money is usually a taboo subject, but I believe that only with transparency can you truly learn and see the ins and outs of what goes into each decision that turns out to be right or wrong. I also believe that much of what I have learned about personal finance and investing has come from seeing how many other people openly share their investments and allow me to learn from what they do.

So today I want to talk about how I bought my first 3-unit apartment at the age of 25 and what I learned from the whole process. And again, I’m not doing this to brag or try to portray a picture that is even the slightest bit different from reality, and I will try to do it as objectively as possible.

My first apartment

In 2021 I had managed to save quite a bit after several continuous years of working at a good salary. The year before, in 2020, I had started investing in the stock market, and in 2018 I had started investing in crypto. In 2021 therefore, after watching a lot of content on YouTube and blogs about investing, I thought it would be a good idea to start diversifying my investment by getting into real estate.

I started looking at apartments both in Almeria (my hometown) and Seville (the city where I live). I started taking courses, watching videos, reading blogs, etc. All the content I saw about real estate investment to try to make a better decision. During this time, my friend Carlos was in a similar situation, and we decided to look together for an apartment to buy between the two of us and rent it.

Then I started to define what I saw as the characteristics of a good investment, which I have been redefining since then:

- A apartment located in a 1st, 2nd or 3rd floor without elevator (less community expenses, practically the same rental price, not worth the extra investment).

- That the building/community is well maintained with good atmosphere and without problems.

- Located in relatively central neighborhoods.

- An area of 50 to 70m2, with 2–3 rooms, with good distribution and as exterior as possible.

- In a state to give it a facelift or to reform directly.

- Ideally a purchase price of between 50.000€ to 70.000€.

- An estimated rent of between 450€ and 550€ per month.

The first apartment we bought was seen by him, advising me that he had directly made a counteroffer at a lower price of 48,000€ for an apartment that was advertised for 55,000€. An apartment located in the center of Almeria, third floor without elevator, with 3 bedrooms and 1 bathroom, 80m2, quite exterior, and that we could easily rent for more than 550€ per month.

The reality is that I did not even get to see this apartment before buying it. It was my partner who went to see it, and by video call we said that it was a good option and that we would make a formal offer. We decided to make the final offer below the first counteroffer, for 46,500€, and, against all odds, it was accepted, pointing out the condition of the property compared to how it appeared in the photos. We made the purchase (and there I finally went to see the apartment in person), and started the renovation.

The condition of the apartment could have been much better, both the floor, walls, windows, electricity, plumbing, etc.. In fact it didn’t even have a kitchen. For all this we knew that although the purchase price of the apartment was cheap we were going to have to make a large investment in the repair of the apartment.

To buy the apartment, we first sign the “arras” contract. This is a contract in which it is agreed between the two parties to carry out the purchase and sale, and also a down payment is paid for the property. In our case, the down payment was 3,000€.

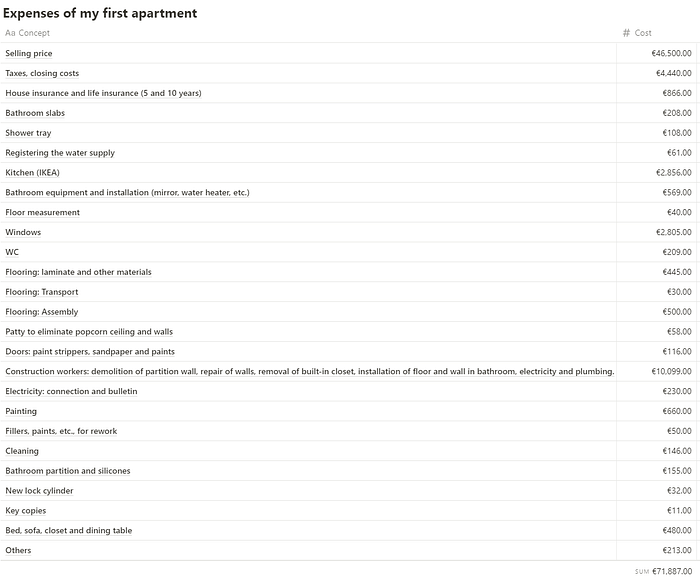

To the purchase price we had to add the renovation costs, which would end up being about 19,600€ (new kitchen and bathroom, knock down a wall, new windows and glass, new flooring, new plumbing and electricity, painting, new appliances and some furniture for the apartment). The details of the cost breakdown are as follows:

Regarding the financing of the apartment, we made a study of several banks and mortgages to choose the one that offered the best conditions. There were several banks that offered us good conditions, however only one gave us 100% financing on the purchase price of the apartment. And I will explain why. The apartment was appraised at 65,000€ once the earnest money contract was signed. This appraisal above the purchase value allowed the bank we chose in the end, Unicaja, to give us 100% of the purchase value, €46,500. However, €8,000 of this was tied to the completion of the renovations we had promised. With this, the bank also ensures that the apartment increases in value, and in case of non-payment and foreclosure, they have a better property at their disposal.

Since they gave us 100% of the price we paid, we did not have to put up even 1€ for the purchase of the apartment (except for taxes and notary fees, which we did pay). This meant that our investment in the apartment was simply to carry out the renovation of the apartment. We split the costs between the two of us, and our individual investment was €10,450 (renovations) + €2,220 (taxes and notary fees) = 12,670€ each.

After finishing the construction work, we put the apartment up for rent. An apartment at the right rental price should not take more than a few weeks to rent. If it does not, it means that we are renting the apartment above the average price for the area. One way to calculate the rental price (and this should be done before buying the apartment to know how much we could offer) is to search on Idealista. We can look for properties with similar characteristics (state of renovation, number of rooms, m2 of the apartment, elevator/no elevator, etc.) to the one we are interested in and with this make the calculations.

In our case we saw at the time that the apartments in the area with similar characteristics were rented for around 550€ per month. However, when we went to rent it, we saw that the condition of the apartment was much better than the rest of the apartments in the area (imitation wood flooring, new windows, new kitchen and bathroom, etc.) so we decided that a more appropriate price was 620€.

To determine the profitability of an apartment we make two calculations. One at the beginning, when we visit an apartment, and another one when we have the mortgage conditions available. These two profitability calculations allow us to determine whether we are interested in buying a property or not.

For the first of them, what we call Gross Profitability, in which we divide the annual rent that we are going to receive by the total cost of the property, including taxes and renovation expenses.

In our case, it would be 7,440€ (620€*12) / 71,887€ = 10.35% gross profitability.

With this what we calculate is the gross profitability if we were to buy the apartment without using the mortgage, so that both the cost we pay and what we receive in rent is entirely ours.

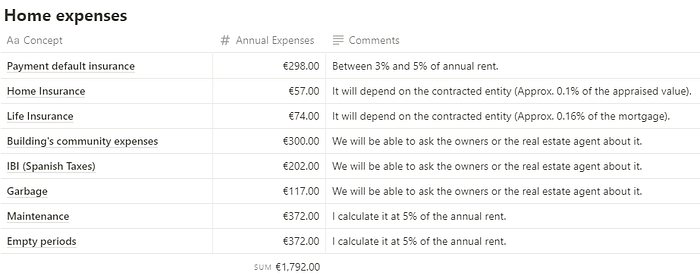

To then calculate the Profit before taxes, some things that we must take into account are the following:

With this data we can calculate the gross profit we would have if we did not have a mortgage but we already have all these expenses present. For this, we subtract this amount from the annual rent received, leaving something like this:

5,648€ / 71,887€ = 7.86% gross profit.

The second profitability calculation we make is on the actual amount we are investing. In our case, as the mortgage was 100%, our investment was the taxes and the renovation of the apartment. To calculate this profitability, we must now also take into account what we paid for the mortgage to deduct it from the amount we receive in rent. With our monthly payment of 279€ per month, it would be 3,352€ of annual mortgage.

In our case, this would be €2,296 (€5,648 — €3,352) / €25,340 = 9.06% gross real return.

We always aim for a gross return of between 8% and 12%, depending on factors such as the neighborhood or the condition of the property, which give us an idea of the risk we are taking. The higher the risk, the better the return should be to make it worthwhile for us. That is why when we offered 46,500€ for the property, it was taking into account that renting at 550€ and about 17,000€ of renovation (which ended up being 21,000€) and looking for a 10% return, we could offer a maximum of those 46,500€.

Before offering a price, in addition to the rental price, we can consult many other data of a given neighborhood in the INE (or other sources), such as average salary, unemployment rate or population growth/decrease in that neighborhood to determine if the apartment will continue to be a good investment over time.

I hope you liked my example of real estate investing and know the numbers behind it. There are many ways to invest in real estate, such as vacation rentals or room rentals, among many others.

Later I will talk about my other real estate investments, some mistakes made in this and other investments and some tricks to get more out of our investments.

Feel free to follow me on The Meerkats to stay tuned for articles on investing, personal finance, entrepreneurship and more!